Overview

This report discusses the issues that impede the development of wind energy in India and undertakes a systematic analysis to propose pathways and interventions to achieve the national target.

Wind energy is India’s oldest and best developed renewable energy technology, and needs to achieve a national target of 60 GW of installed capacity by 2022. However, factors such as frequent policy changes, infrastructural unpreparedness, and a lack of consensus among stakeholders have crippled the growth of the sector, thereby jeopardising the possibility of achieving these targets in time.

This report presents the current state of the sector in terms of capacity additions and lists policy changes and other factors that have led to the current scenario. It incorporates a detailed assessment of different approaches to achieve the national target. The report also provides various state-specific scenarios and compares them on multiple grounds, highlight the associated challenges for each. It proposes some optimum approaches to achieve the 2022 target.

Key Findings

Impediments to growth

- Most of the land in the high wind regions with access to grid connections have been used up, therefore, augmenting existing substations or building new ones is essential for setting up new wind power plants.

- There is a need to expand the transmission network to keep up with the deployment of new capacity, as this will ensure effective evacuation of the energy generated by wind power plants.

- There is a need of an effective mechanism for regional cooperation that would enable the seamless exchange of power, as an effective framework would facilitate the inter-regional and inter-state exchange of power.

- The poor financial condition of distributing companies (discoms) has resulted in payments to wind power producers being delayed, thus creating cash flow problems for power producers which are at risk of being classified as non-performing assets (NPAs).

- Wind power developers are facing serious challenges in implementing the reverse auction process. They are facing delays in procuring land and gaining connectivity to the inter-state transmission system (ISTS) network.

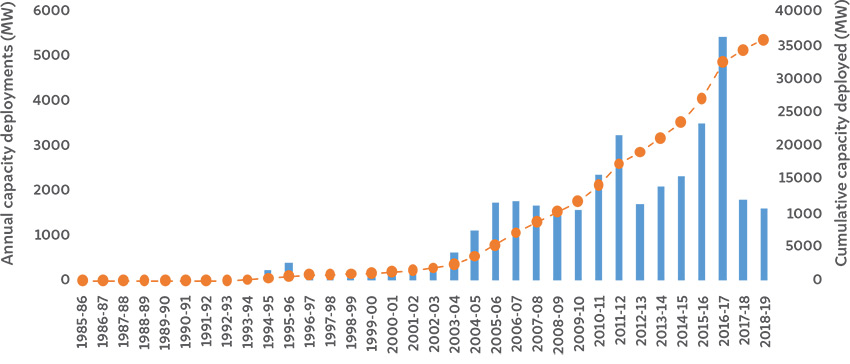

Annual wind capacity additions

Source: Ministry of New and Renewable Energy (MNRE)

Three Case Scenarios

This report provides three case scenarios to achieve the 60 GW target by 2022:

Scenario 1: Base Case

- Integrating wind power in large-scale into the grid could cause voltage and frequency fluctuations, due to which the grid gets destabilised, power quality degrades, and the power system may breakdown.

- Development of transmission infrastructure for renewable electricity transmission is not in line with the development of the renewable sector.

- To facilitate the procurement of suitable land with connectivity to the grid, the development of designated wind parks would be essential.

Scenario 2: Low-medium Wind Power Density (WPD) sites

- This scenario explores the potential to locate more capacity in medium-low WPD sites and it assumes the use of fallow and agricultural land for wind energy generation.

- The higher capacity in medium-low WPD sites will result in a higher levelised cost of electricity (LCOE) and lower energy production.

- Deploying new capacity in medium-low WPD sites would lead to higher tariffs for the energy generated compared to the current ceiling tariffs and solar photovoltaic (PV) tariffs.

Scenario 3: Repowering of old power plants

- There is at least 1.6 GW of repowering potential between five states – Tamil Nadu, Maharashtra, Gujarat, Andhra Pradesh, and Karnataka – if the turbines installed before 2002 are considered for repowering.

- LCOE is estimated only for new capacity as the LCOE of the repowered capacity would vary significantly based on its age, location, ownership, etc.

- There is a need for new business models and tariff designs to incentivise existing developers and CPP owners to repower old plants.

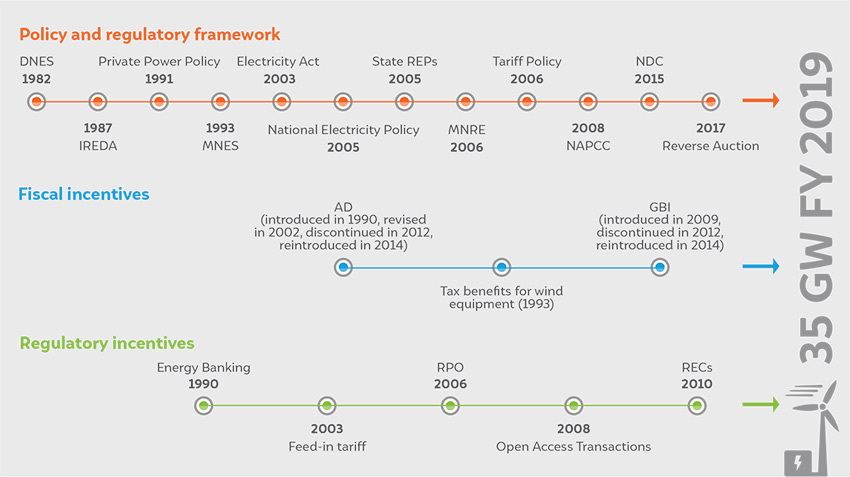

Timeline of policy interventions and incentives

Source: Authors’ analysis

Key Recommendations

- Distribute the capacity from high to medium and low WPD regions. Repowering old wind plants is also an option to increase capacity.

- Quantify the trade-offs between the different approaches, develop a long-term strategy, and back it up with policy, regulatory, and budgetary support.

- Define a clear policy objective after carefully choosing from the multiple approaches to deploy new capacity. Also, undertake an accurate assessment of the overall cost of adopting each of the approaches

- Streamline the reverse auction process for deploying new capacity at the central and state level as well as optimise the scaling up of the wind energy sector so that it offers the maximum economy-wide benefits.

- Provide regulatory support to create and sustain demand in the sector. Revise open-access regulations across states to streamline the application process and prevent additional charges from reducing the competitiveness of wind energy.

- Develop regulatory and financial mechanisms to address the high off-taker risk in the sector. Deploy financial de-risking mechanisms such as Grid Integration Guarantee (GIGs) to reduce the wind curtailment risk.

- Deploy innovative financial mechanisms such as green bonds, which can be issued by the states and used to finance working capital loans to meet the renewable purchase obligation of distribution companies.

- Create a robust ancillary services market with innovative market designs that can facilitate better integration of RE while minimising the impact of grid balancing on the efficiency of conventional plants.