Council on Energy, Environment and Water Integrated | International | Independent

Issue Brief

Mapping India’s Residential Rooftop Solar Potential

A bottom-up assessment using primary data

Sachin Zachariah, Bhawna Tyagi and Neeraj Kuldeep

November 2023 | Energy Transitions

Suggested citation: Zachariah, Sachin, Bhawna Tyagi, and Neeraj Kuldeep. 2023. Mapping India’s residential rooftop solar potential A bottom up assessment using primary data. New Delhi: Council on Energy, Environment and Water.

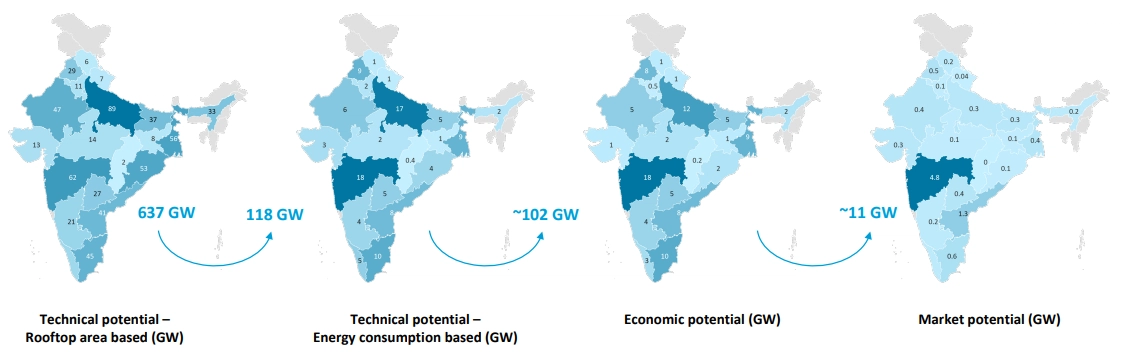

CEEW conducted a detailed assessment of the technical, economic, and market potential of deploying rooftop solar (RTS) in Indian households by adopting the bottom-up approach. i.e. starting at the household level. The study utilises the primary data collected in India Residential Energy Survey (IRES) of 14,850 households spanning across 21 states and 152 districts in 2020. The assessment further provides insights into the RTS potential of different states, the urban-rural split, and the potential for different system sizes.

Rooftop solar provides an opportunity for households to contribute significantly to the ongoing energy transition by substituting their electricity consumption with solar. The true economic and market potential can be captured only by considering households’ economic strength and energy footprint.

Key Highlights

National-level estimations:

Technical potential reduces to one-fifth when the system size is restricted to meet households’ electricity consumption due to lower electricity consumption per square feet (sq ft).

In total, 85 per cent of the technical potential is concentrated in RTS systems size between 0-3 kilo watt (kW) as electricity consumption across states in India is concentrated in the lower slabs.

In total, approximately 30 per cent of the technical potential lies in the 0-1 kW category. However, this category is not recognised in policy and subsidy schemes.

The decline in technical potential is higher in rural areas due to low electricity demand per sq ft (6.8 kWh per sq ft) compared to urban areas (7.7 kWh per sq ft).

The Ministry of New and Renewable Energy (MNRE) subsidy 1 is effective for an RTS system size of 1-3 kW, and can increase the economic potential by ~5 GW by making systems economically feasible for more consumers with no change in system sizes above 3 kW.

Source: Authors' analysis

State-level estimations:

More than 60 per cent of the technical potential is concentrated in seven states in India.

A significant decline in technical potential is witnessed in states such as Assam, Bihar, Odisha, Madhya Pradesh, Rajasthan, Jharkhand, and Uttarakhand due to the large share of households with low energy consumption per sq ft.

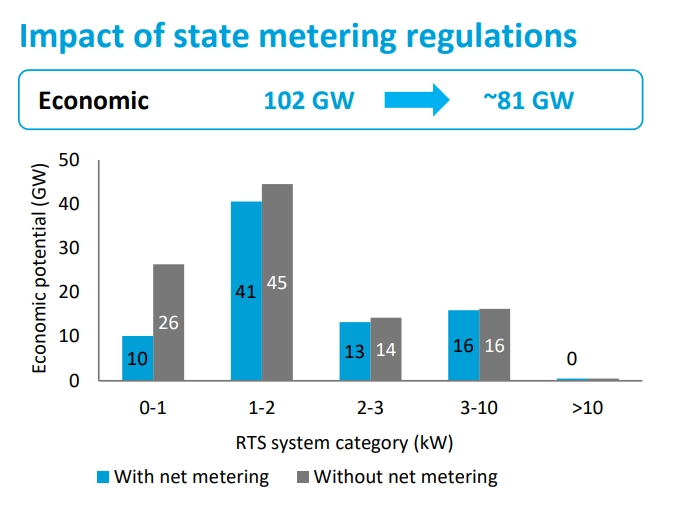

Net-metering regulations further reduce the economic potential from about 102 GW to about 81 GW due to minimum kW restriction limits for RTS in 15 states. For West Bengal, the potential reduces to zero due to a minimum limit of 5 kW.

Flat MNRE capital subsidies increase the economic potential in states by making systems economically viable.

Consumer awareness about solar is less than 60 per cent in most of the states. Awareness in urban areas is only 6 per cent higher than rural areas. Consumers in most states find RTS systems to be costly, making them averse to buying them.

Key Recommendations

Introduce targeted capital subsidies, particularly for RTS systems of size 0-3 kW to maximise economic potential and ensure the economic viability of different RTS system sizes.

Recognise RTS systems of <1 kW, both in policies and regulations, as significant potential lies in this category.

Roll out a national awareness campaign is crucial to generate a more significant demand for RTS.

Develop a one-stop platform for consumers at the state level to receive credible information about RTS. The intent is to provide consumers with easy access to basic, reliable, and compelling information.

Unlock untapped potential by moving beyond traditional models to overcoming constraints such as limited roof space, ownership of roofs, and capital constraints.

Introduce low-cost financing options with a fast approval process and a separate line of credit for residential consumers.

FAQs

What is the residential rooftop solar capacity in India?

According to Bridge to India’s Solar Rooftop Map (June 2023), the residential rooftop solar installed capacity in India is 2.7 GW.

What is India’s rooftop solar target?

India has set a target of 40 GW of rooftop solar by 2022, out of which ~11 GW has been achieved as of 31.10.2023.

What are the benefits of rooftop solar?

Rooftop solar can help consumers save on their electricity bill with the use of available roof space. It also provides residential consumers access to reliable and clean electricity and an opportunity to contribute significantly to India’s energy transition. Rooftop solar also reduces T&D losses as the points of electricity generation and consumption are colocated.

How much does rooftop solar cost in India?

What is the payback period for rooftop solar in India? The MNRE-notified benchmark cost of a rooftop solar system of size 1 - 2 kW is INR 43,140 per kW (excluding GST), applicable for general category states/ UTs. The payback period for rooftop solar in India will vary based on the system size, electricity generation and consumption, subsidy availed and so on. The study considers a payback period of less than 5 years to estimate the market potential.

Is there a rooftop solar scheme in India?

MNRE has a grid-connected rooftop solar program. The program currently in its second phase which has been extended till 31.03.2026.

“Capitalising on the rooftop solar potential, particularly in the <1 kW category, requires changes in regulations, policies and supported by the roll out of innovative business models.”